I hate being ripped off by high street banks (or any other financial institution for that matter) when I spend money abroad. Being honest though, despite being a lifelong traveller and nomad who should have known better, as a result of not really caring too much when I was younger, combined with a distinct lack of better foreign spending options, I’ve probably contributed to a few Christmas bonuses for those financial fat cats in my time!

The simple fact is this – if you still travel using your high street bank account and card to pay for things and withdraw money, then you’re certainly losing many dollars, pounds or euros to your bank with each trip abroad you take.

What has changed though in recent years, is the emergence of several progressive financial fintechs which tackle this exact problem. Some of which have totally revolutionised how to spend money when travelling.

So if you want to avoid unnecessary ATM and foreign exchange fees, as well as the hassle of managing different currencies while overseas, then choosing the right travel bank account makes all the difference.

In this article, I’m sharing my experiences of being a long-term user of three of the best bank accounts for travelers and nomads: namely Wise, N26, and Revolut. I want to help you decide which is best for your specific travel and lifestyle needs, as I’m convinced that simply switching up your travel spending habits will save you money, time and stress.

So, sit back, put that sandwich down (cos lunch is for wimps here in the city ;-)) and let’s have a Wise vs Revolut vs N26 financial battle royale…

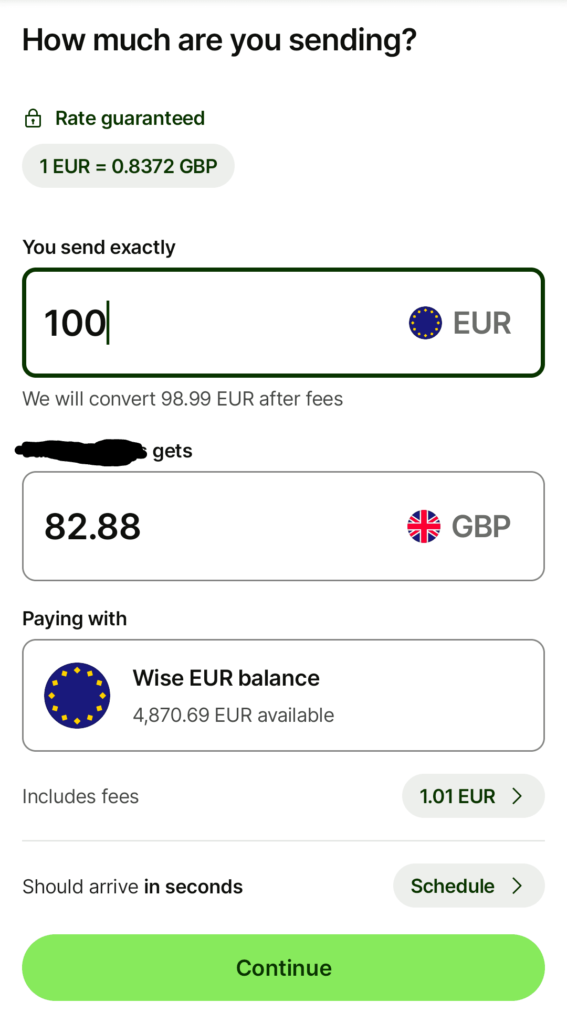

Wise (formerly TransferWise) is best known as somewhere people go when they want to change money from one currency into another. But beyond single currency exchanges and transfers, they also offer multi-currency accounts that allow users to hold, receive, and send money in over 40 currencies, all at the real mid-market exchange rate (i.e the exchange rate you see on Google).

This makes it a top choice for travelers who frequently switch between currencies, or even digital nomads who are paid in multiple currencies, and want to avoid hidden fees whenever converting between them.

Wise Benefits

Multi-currency account: When you open a Wise account you’re given bank details for several different currencies (you choose which ones you need). In theory, this means you can hold and convert over 40 currencies, although you’re a bit dodge if you need this many!

Move your money between currencies when exchange rates are favourable: If you’re savvy and like to keep an eye on the exchange rates, moving your money between the different currencies you hold with Wise at the right time can not just save you money, but also earn you money.

Mid-market exchange rates: Wise offers the real mid-market exchange rate without any markups, this makes them very hard to beat on price, as all you are paying is a small fee on each transfer.

Generous interest rates: Wise users have the option to earn interest on positive balances by investing in low-risk funds (government-secured bonds).

Pay bills easily: set up direct debits and other regular payments with both personal and business accounts.

No hidden fees: Transparent pricing model with their fee clearly displayed before any transaction. Fees are kept separate, and not bundled into the cost of the currency exchange which I really like, as it makes it much easier to see the actual cost I’m paying.

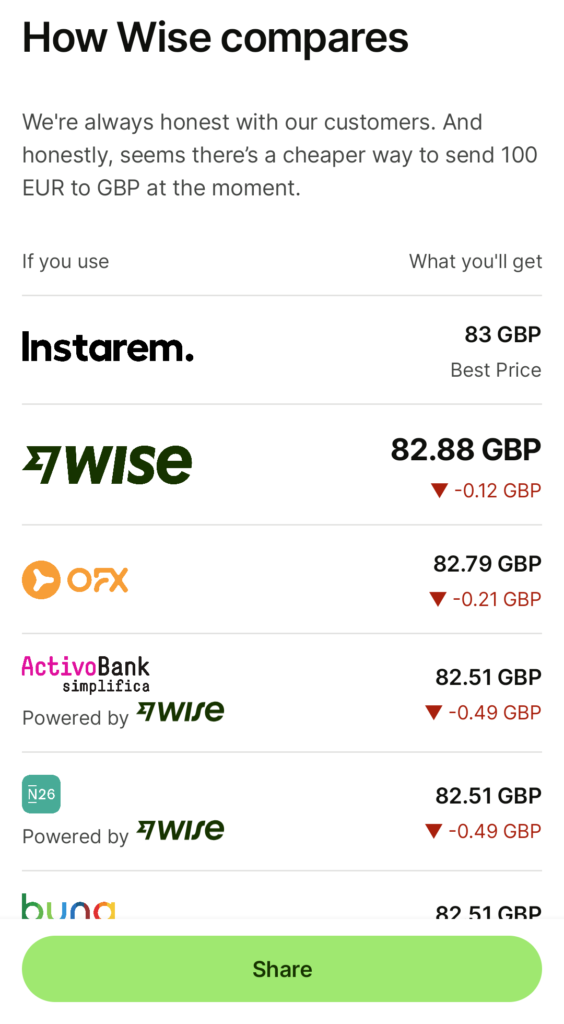

Honesty: As the original FX fintech upstart, Wise love to show how their fees and rates compare with the opposition. They do this even when narrowly beaten by 12 cents! (see photos). Gotta love this truly refreshing approach from a financial institution.

Free digital debit card: You can use the Wise debit card for spending in multiple currencies, and it automatically converts at the best rate available. You can also link it with your mobile wallet (Google or Apple Pay).

Invoice customers in their native currency: If you’re a business owner with clients from all over the world, the Wise Business Account enables you to bill them in their local currency, potentially increasing conversion rates. The specialist ‘Invoices’ section makes this super easy in fact.

Wise Drawbacks

Limited functionality: Unlike Revolut and N26, Wise focuses primarily on currency exchange and lacks some of the more traditional banking features, like overdrafts or loans. But if you always stay in the positive, then this certainly isn’t much of a negative.

No physical debit card as standard: You can get a physical card to use at ATMs, but you have to pay approx 10 bucks (EUR/$) for it.

ATM withdrawal fees: Free withdrawals are limited to €200 (or equivalent) per month, after which a small fee (0.50 EUR) is charged per withdrawal, so again, not exactly a deal breaker here.

REVOLUT

Revolut positions itself as a one-stop financial solution, offering not only currency exchange but also budgeting tools, savings features, and even cryptocurrency trading. It’s ideal for travelers who want more than just currency conversion and who need to manage their finances on the go.

Revolut Benefits

Multi-currency account: Similar to Wise, with Revolut you can receive, keep, and exchange 30+ currencies worldwide, with their multi-currency bank account. Users apply for local account details, depending on their requirements.

Budgeting & spending insights: Track spending across different categories, set budgets, and get insights into your financial habits.

No fees for international spending: Want to buy that croissant in Paris with pounds? No worries – you won’t be charged any additional fees by Revolut, just their currency exchange fee.

Travel & lifestyle perks: Depending on their account tier (free, Plus, Premium, Metal, and Ultra) Revolut users earn ‘RevPoints’ on debit card spends. These can then be traded in for Airmiles with different airlines, discounted accommodation, discounts on things to do, and other non-travel based rewards. Free standard accounts earn 1 point for every £10 spent, and this increases all the way up to 1 point per £1 spent with their premium ‘Ultra’ account.

Revolut Drawbacks

Exchange rate markups on weekends: Revolut adds a small markup (approx 1%) on their currency exchange rates on the weekend. I’m not sure why they figure that people should pay more on Saturdays and Sundays, but regardless, this will obviously lead to higher costs if you’re converting large sums.

Lack of transparency with fees: In addition to the above point, some other fees can be confusing, especially for ATM withdrawals.

No overdrafts offered: Despite wanting to position itself as a holistic answer to travel banking, Revolut do not currently offer overdrafts with ANY of their accounts. So for those of you who need to dip below zero from time-to-time, this might be a factor worth considering.

N26

N26 is a digital bank, originating in Germany that has since expanded to most other European countries. Until 2020 and 2022, it was also operational in the UK and the US respectively, but all non-European operations have long since ceased. This is a real shame, as I’ve been using N26 for over 10 years now and I have nothing but good things to say about my experiences with them.

Unlike Wise and Revolut, N26 operates much more like a traditional bank, providing features like direct deposits, overdraft facilities, and comprehensive spending analytics.

N26 Benefits

Full-service banking: Includes traditional banking features like direct debits, overdrafts, and savings options. Premium users also get travel insurance and airline lounge access.

Cash 26: For accounts opened in Germany, Spain and Austria, users can withdraw and deposit cash in thousands of local retail stores, simply by generating a barcode in the app. Retail staff then scan this and your withdrawal or deposit is then immediately updated in your account.

CASH26 effectively removes the need for both a debit card and any ATM machine (assuming the shops are still open!). CASH26 deposits are charged at 1.5% of the total amount, but the withdrawals are free. I regularly use CASH26 for withdrawing money, and it has saved my butt on many occasions!

Free basic account option: The N26 Standard account has no monthly fee, yet still provides many benefits, including fee free payments in any currency, and no minimum deposit requirements.

User-friendly app: The N26 app is sleek, easy to use, and provides real-time spending notifications.

European banking license: Money in N26 is protected up to €100,000 by the German Deposit Protection Scheme.

N26 Drawbacks

This is not a multi-currency account: N26 deals only in EUR, so if you want to hold more than one currency you’ll need to open a separate account with a different provider.

Not available in the UK or the US: This is a pretty big one unfortunately. N26 is solely focused on its core European markets, so if you’re resident in the EU or an EEA country, good for you, if not, then Wise or Revolut it is!

COMPARING FEATURES

| Feature | Wise | Revolut | N26 |

|---|---|---|---|

Availability | Worldwide | Europe, US, Australia, Asia | EU, EEA countries only |

Monthly Fee | No monthly fee | Standard (Free), Plus (€3.99/£3.99/ not available in US), Premium (€8.99/£7.99/$9.99), Metal (€15.99/£14.99/$16.99), Ultra (€60/£45/not available in the US) | N26 Standard (Free), N26 Smart (€4.90), N26 You (€9.90), N26 Metal (€16.90) |

Currencies Supported | 40+ | 30+ | Primarily Euro, USD, GBP |

Exchange Rates | Mid-market rate | Mid-market on weekdays, markup on weekends | N26 have partnered with Wise for their currency exchanges, so a slight markup on Wise rates |

ATM Withdrawal Limit (Free) | 2 free withdrawals per month, up to a total of €200. 1.75% on any amount thereafter. After your two free withdrawals you'll also be charged 0.50 EUR fee per withdrawal | Up to €200/month or 5 withdrawals (on the free plan), higher for premium accounts | Limited for 3 withdrawals per month in most European countries on the free account, free unlimited withdrawals from N26 You and Metal |

Additional Features | Multi-currency account, digital and physical debit card, can use the digital card with Google Pay and Apple Pay | Budgeting, travel insurance, international stock trading, cashback offers | Full banking services, travel insurance, overdraft facility, crypto, EFTs & stocks investing |

Card | VISA or Mastercard debit card | VISA or Mastercard debit card | Mastercard debit card |

Interest Paid | Returns on EUR (3.24%), GBP (4.46%) and USD (4.74%) balances | Depending on which plan you choose, up to 4.75% on £ accounts, up to 4.25% on $ accounts, and up to 2.12% on € accounts | 1.7% on Standard (free) & Smart accounts, 2% on N26 YOU, and 3% with N26 Metal |

WHAT EACH ACCOUNT IS BEST FOR?

Choose N26 if you’re based in Europe (but not the UK), and if you prefer/need a full-service digital bank that can replace your traditional bank account. N26 is best for travelers who want a mix of banking features, like an overdraft, loans, fee-free payments abroad, and premium benefits like travel insurance.

Choose Wise if you frequently convert between multiple currencies, and you want close to market-leading exchange rates with no hidden fees. It’s also a great choice for freelancers, remote workers, and long-term travelers who manage their money across borders, and who get paid in multiple currencies.

Bottom line: if you regularly receive and spend in more than one currency, you’d be crazy not to have an account with Wise. Digital nomads in particular should consider a Wise Business Account, as they can take care of multiple payments, back home or elsewhere, at the best rates available.

Choose Revolut if you’re looking for an all-in-one financial app that offers not just currency exchange, but also budgeting tools, travel insurance, and various investment strategies, including crypto trading!

The various account tiers available with Revolut means you can choose a plan that fits your budget, needs and your travel style. Revolut seems to cover the needs of tech savvy generations and modern travellers as well as any other Fintech out there.

WISE VS REVOLUT VS N26: CONCLUSION

Look, there’s no reason why you shouldn’t have all of these accounts. While that entails a little bit more personal admin, it is worth keeping in mind that Wise, Revolut, and N26 each bring their own unique strengths to the table.

Wise excels at providing transparent and market leading currency exchange rates. Revolut offers a wide array of financial tools for tech-savvy travellers and digital nomads, and N26 brings a comprehensive digital banking experience for European residents.

As a Brit living in Europe, with clients from all over the world, I personally use a Wise Business Account, an N26 account for day-to-day living here in Austria, and Revolut when I visit family and friends back in the UK. With this combo, I’m saving myself thousands in fees each year, and I find it very simple to manage all three together.

Your own choice will ultimately depend on your own travel habits, where and how you get paid, your financial needs, and of course, where you live. Thanks for reading, and if you have any of your own thoughts on Wise, N26, or Revolut then leave a comment below.

Happy travelling!

Great article,Very helpful and well-written. Thanks

Thanks very much, Rose – glad you found it useful!